HSA vs. METC: How to Save Thousands on Medical Expenses

How Ontario Small Business Owners Can Save Thousands on Medical Expenses

Paying for medical expenses out-of-pocket can feel like a never-ending drain on your wallet. The good news? Canada’s tax system offers two ways to soften the blow: the Medical Expense Tax Credit (METC) and Health Spending Accounts (HSA).

Both can save you money — but one of them is a game-changer if you’re an incorporated business owner in Ontario. Let’s break it down.

What Is the Medical Expense Tax Credit (METC)?

The METC is a non-refundable tax credit you can claim on your personal tax return.

- Non-refundable means it can lower the tax you owe, but it won’t give you a refund beyond that.

- You can claim eligible expenses such as prescription drugs, dental care, certain medical devices, and professional health services.

- You can claim any 12-month period ending in the current tax year — but only once.

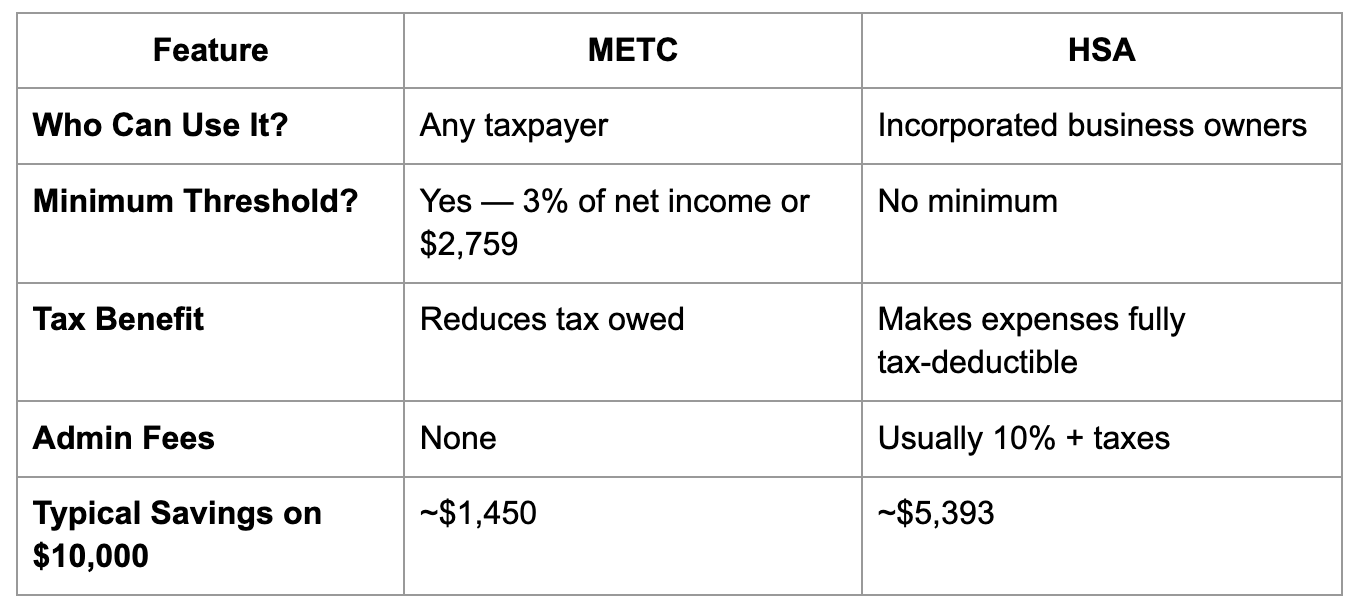

- The catch? You can only claim expenses that exceed the lesser of 3% of your net income or $2,759 (for 2024).

How the METC Works in Ontario

Here’s a real example for an Ontario resident:

Net Income: $100,000

Eligible Medical Expenses: $10,000

Ontario’s Lowest Marginal Tax Rate: 5.05% (federal lowest rate is 15%)

Step-by-step:

- 3% of $100,000 = $3,000

- Compare $3,000 with $2,759 → lower is $2,759

- $10,000 − $2,759 = $7,241

- Multiply $7,241 by the combined lowest federal + provincial tax rate (15% + 5.05% = 20.05%) → $1,450.42

Result: Your non-refundable credit is $1,450.42.

That’s something — but what if you could make the entire $10,000 tax-free?

What Is a Health Spending Account (HSA)?

A Health Spending Account is CRA-approved and allows incorporated business owners to turn 100% of their personal medical expenses into before-tax business expenses.

In other words: your company reimburses you for medical costs, the reimbursement is tax-free for you, and your company deducts it as an expense.

It’s like paying for braces, dental work, or physiotherapy with pre-tax dollars.

HSA Savings Example – Ontario

Let’s use the same $10,000 in medical expenses.

Marginal Tax Rate: 43% (typical for someone earning $100,000 in Ontario)

Admin Fee: 10% = $1,000

Applicable Taxes:

- HST (13%) on admin fee = $130

- RST (8%) on claims = $800

- PST (2%) on claims + admin fee = $220 (2% of $11,000)

Without an HSA:

- You’d need to earn $17,543 in gross income to have $10,000 left after tax to pay the bill.

- $7,543 of that is tax.

With an HSA:

- Your company pays:

- $10,000 medical claim

- $1,000 admin fee

- $130 HST (on admin fee)

- $800 RST (on claims)

- $220 PST (on claims + admin fee)

- Total cost to the company: $12,150

- You pay $0 in personal tax on the reimbursement.

The Savings

$17,543 − $12,150 = $5,393 saved — a 30.7% reduction in cost.

METC vs. HSA – Which Wins?

Bottom line: METC helps, but HSA supercharges your tax savings if you’re incorporated.

Why Many Ontario Small Business Owners Choose an HSA

- Immediate Savings: Turn personal expenses into business deductions instantly.

- No Minimums: Claim every eligible dollar.

- Broad Coverage: Includes dental, vision, physio, massage, prescriptions, and more.

💡 Important: You can’t claim the same expense for both the METC and an HSA — you have to choose one.

Final Word

If you’re an incorporated business owner in Ontario, a Health Spending Account (HSA) can save you thousands more than the METC. It’s one of the most effective (and CRA-approved) strategies to reduce your tax bill while covering essential healthcare costs.

Subscribe

Join our newsletter and stay updated with the latest news and insights from our team.

Build your plan for free

Get started today by building your plan. No upfront payments. No long-term commitments. Entirely pay-as-you-go. You won't incur any costs until your team submits a claim.